Before you fall in love with a home, and even before you start looking at homes, take the time to figure out the right monthly payment for your budget. Even if you’ve been prequalified for a mortgage loan amount, check to make sure what mortgage payment will fit within your lifestyle without putting important financial plans on hold.

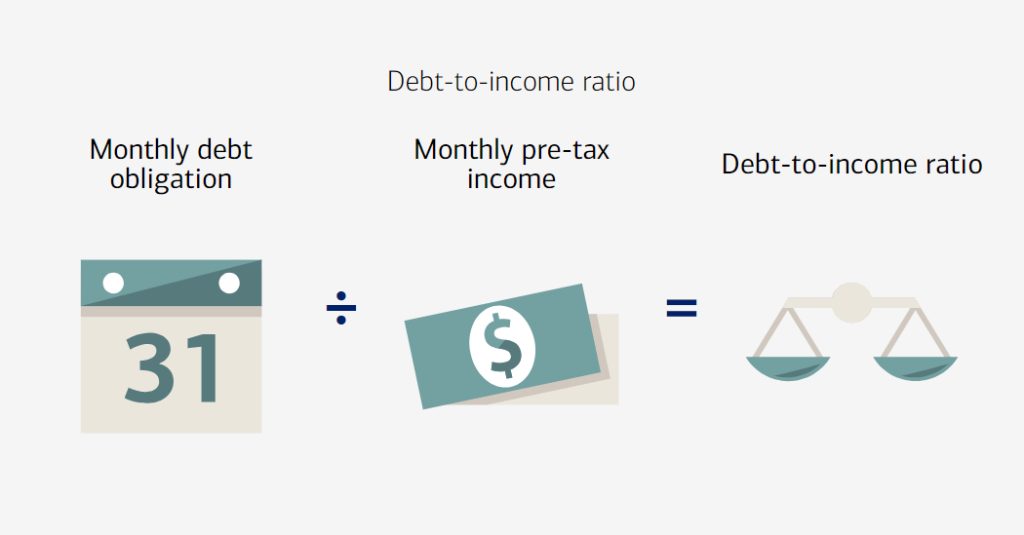

How to calculate your debt-to-income ratio

Lenders calculate your debt-to-income ratio by using these steps:

1) Add up the amount you pay each month for debt and recurring financial obligations (such as credit cards, car loans and leases, and student loans). Don’t include your rental payment, or other monthly expenses that aren’t debts (such as phone and electric bills). And unless you are keeping the home you currently own, don’t include your current mortgage.

2) Add your projected mortgage payment to your debt total from step 1.

3) Divide that total number by your monthly pre-tax income. The resulting percentage is your debt-to-income ratio.

Most lenders want your debt-to-income ratio to be no more than 36 percent, but some lenders or loan products may require a lower percentage to qualify.

Lowering your debt-to-income ratio

If you find your DTI is too high, consider how you can lower it. You might be able to pay down your credit cards or reduce other monthly debts. Alternatively, increasing the amount of your down payment can lower your projected monthly mortgage payments. Or you may want to consider a less expensive home.

You could also lower your DTI by increasing your income. Some lenders may take into account nontraditional sources of income such as alimony, military or work housing stipends, or a trust income. If you have nontraditional sources of income, be sure to ask your lender about the availability of mortgage products and programs that include them.

In addition to lowering your overall debt, it’s important to add as little, or no, new debt as possible during the homebuying process such as buying a car or opening a new credit card.

Keeping your debt-to-income ratio low can help you qualify for a home loan and pave the way for other borrowing opportunities. It can also give you the peace of mind that comes from handling your finances responsibly.